Market Summary 2Q–2026

Broadening Leadership: Markets Look Beyond the Magnificent Seven

The second quarter of 2026 served as a reminder that bull markets don't require the same companies to lead forever.

Just three months ago, investors worried that if the Magnificent Seven technology stocks faltered, the broader market would inevitably follow. Instead, the exact opposite occurred. While the largest technology companies have recently paused after years of extraordinary performance, the rest of the market has quietly stepped in to carry the load.

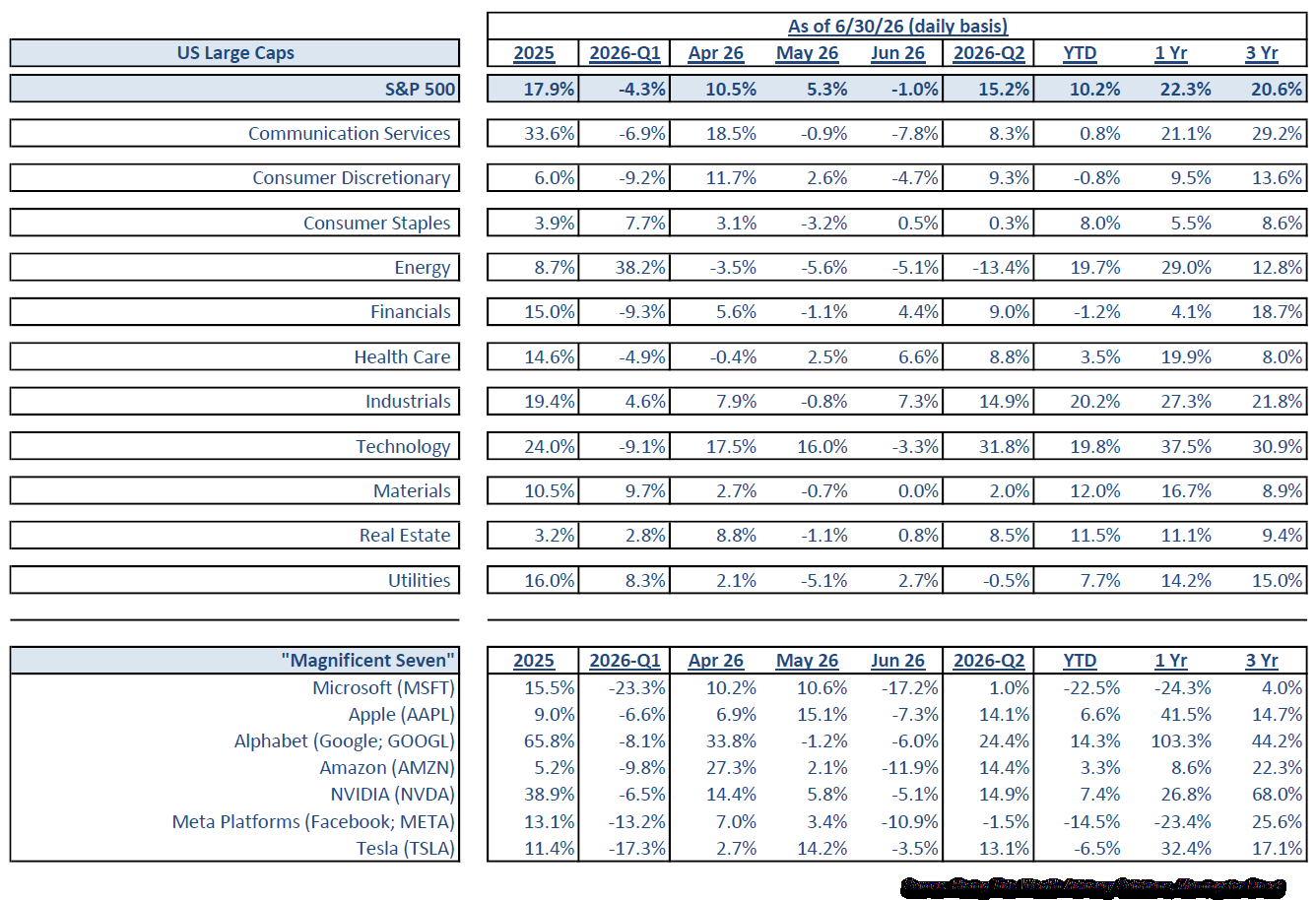

The S&P 500 gained an impressive 15.2% during the second quarter and now stands 10.2% higher for the year. What makes this rally particularly encouraging is not simply the magnitude of the gains, but how much broader they have become.

Technology remained the strongest sector during the quarter, advancing 31.8%, but leadership expanded well beyond a handful of mega-cap names. Consumer Discretionary, Financials, Healthcare, Real Estate, and Communication Services all posted strong gains as investors found opportunities across a much wider range of industries.

Perhaps most encouraging has been the participation from smaller companies. The Russell 2000 gained 21.5% during the quarter, significantly outperforming the S&P 500. Historically, expanding market participation has often been a sign of a healthier bull market rather than a weaker one.

Ironically, this broadening of leadership has occurred even while many investors worried that the market's biggest winners were beginning to lose momentum.

History Says Leadership Always Changes

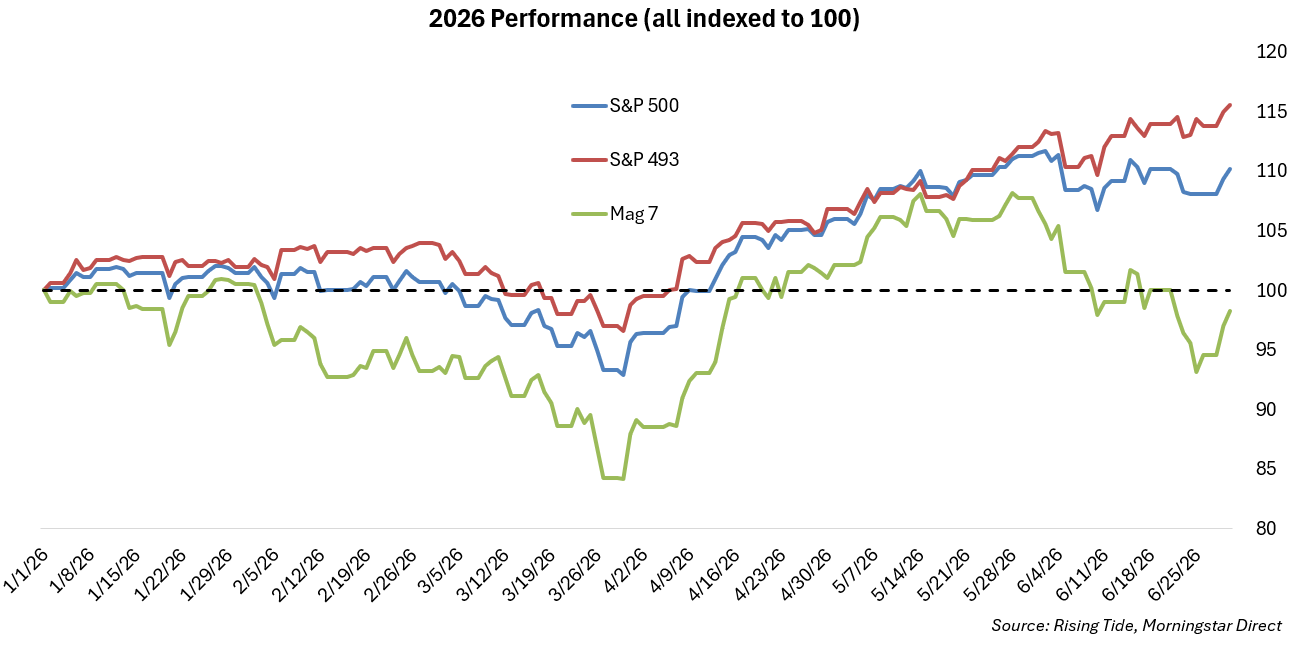

One of the more interesting developments during the quarter has been the changing makeup of market leadership.

Since roughly the middle of May, returns have become less dependent on the Magnificent Seven stocks that dominated headlines over the past several years. Instead, many of the other 493 companies in the S&P 500 have begun contributing more meaningfully to overall index performance.

This should not be viewed as a negative development. History repeatedly shows that market leadership evolves as new technologies mature. During the Industrial Revolution, leadership shifted away from companies building electricity toward companies using electricity. During the internet boom, enormous value was eventually created not only by the infrastructure providers, but by businesses that successfully adopted the technology.

Artificial intelligence appears to be following a similar path.

While Nvidia remains one of the defining companies of this investment cycle, investors have increasingly begun rewarding the "second wave" beneficiaries of AI infrastructure. Memory chip manufacturers such as Micron, SanDisk, and SK Hynix have emerged as significant winners as hyperscalers continue building data centers. Even Intel has benefited as investors gain confidence in its turnaround strategy and expanding semiconductor foundry business.

The biggest companies matter—until they don't. Eventually, nearly every market cycle experiences a passing of the baton. Diversified investors should not be surprised if, several years from now, the names dominating today's headlines look very different.

Fundamentals Continue to Improve

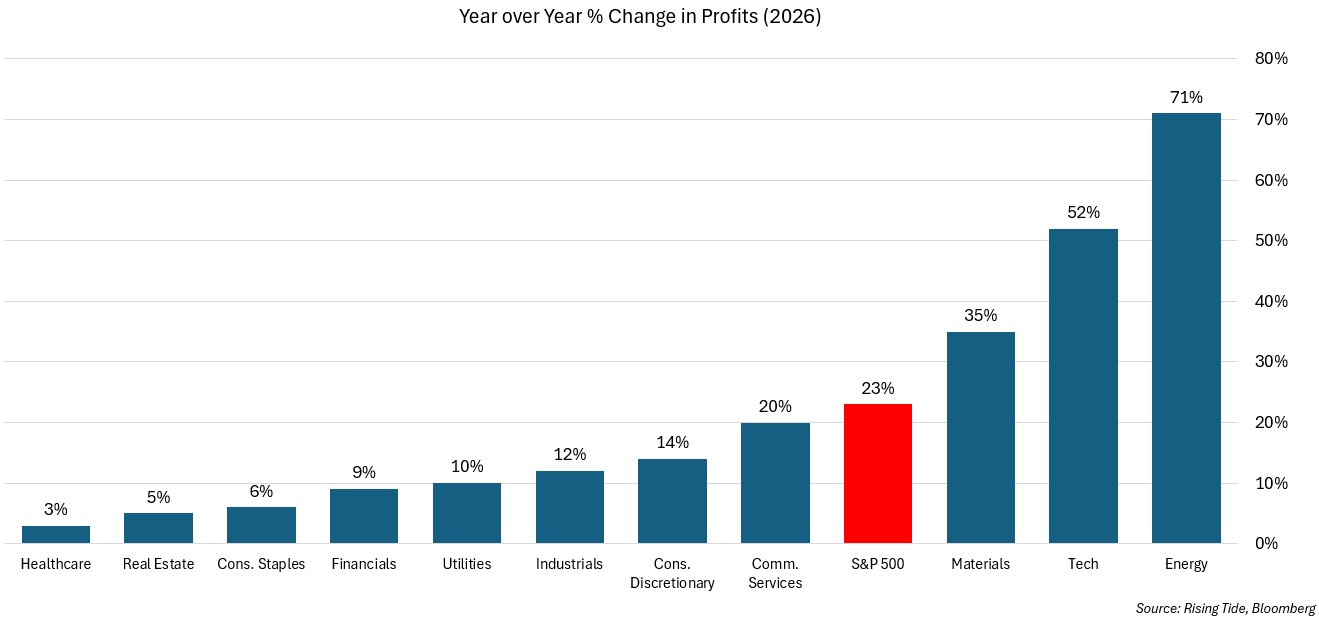

Ultimately, stock prices follow corporate profits. One reason markets have continued climbing despite ongoing geopolitical uncertainty is that earnings expectations have improved meaningfully.

Consensus estimates now call for S&P 500 earnings to grow approximately 23% during 2026, with every major sector expected to contribute. Profit growth this broad has not been seen since 2018.

Of course, these remain estimates. One of the biggest mistakes investors make is treating Wall Street forecasts as guarantees. They are educated expectations based on the information available today. Wars begin. Pandemics emerge. Recessions develop. Markets constantly adjust to new information.

In reality, earnings expectations often follow stock prices rather than lead them. Analysts become more optimistic after companies perform well, just as they become more pessimistic during downturns.

Nevertheless, today's earnings outlook provides a fundamentally sound explanation for why stocks have continued reaching new highs. Markets discount tomorrow's economy, not today's headlines.

The Economy Remains Resilient

The economic picture also improved modestly during the second quarter.

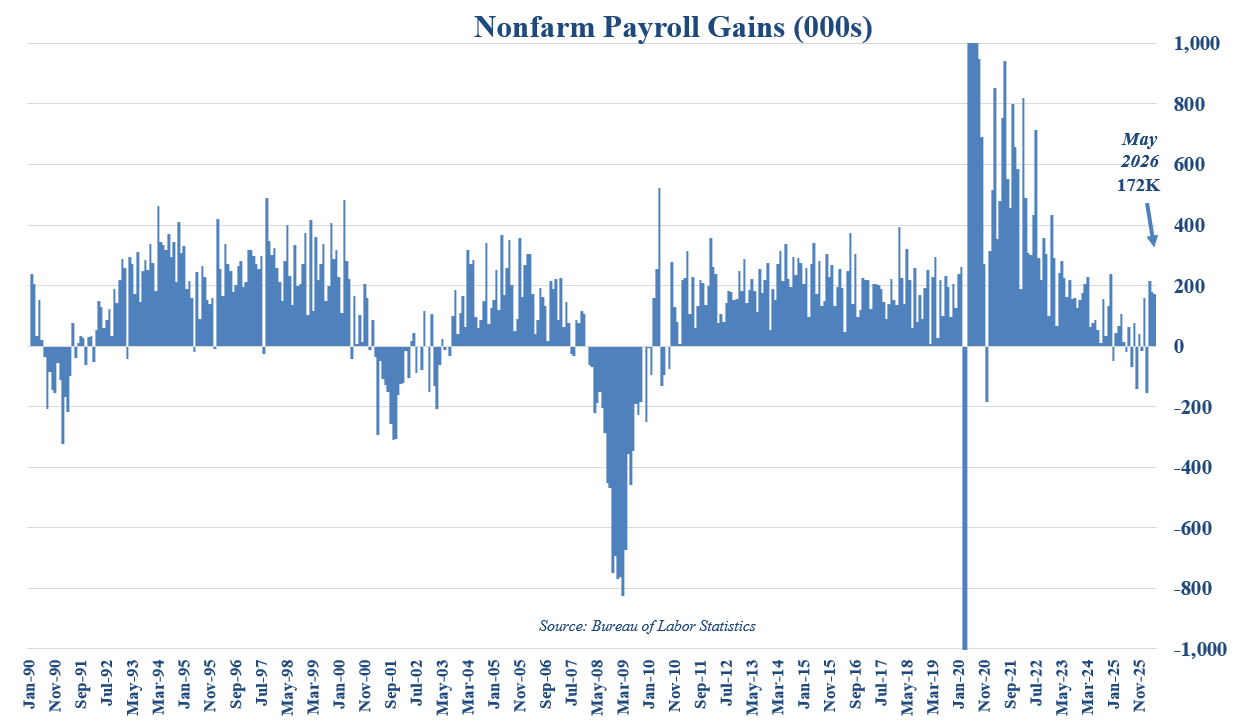

Payroll growth rebounded after an extended stretch of weak employment reports. Employers added 214,000 jobs in March, followed by 179,000 in April and another 172,000 in May, suggesting hiring has regained some momentum.

Other labor statistics tell a more nuanced story. The unemployment rate improved to 4.3%, but labor force participation continued drifting lower as fewer Americans actively sought work. In other words, while the labor market has stabilized, it is probably not as strong as the headline unemployment rate alone would suggest.

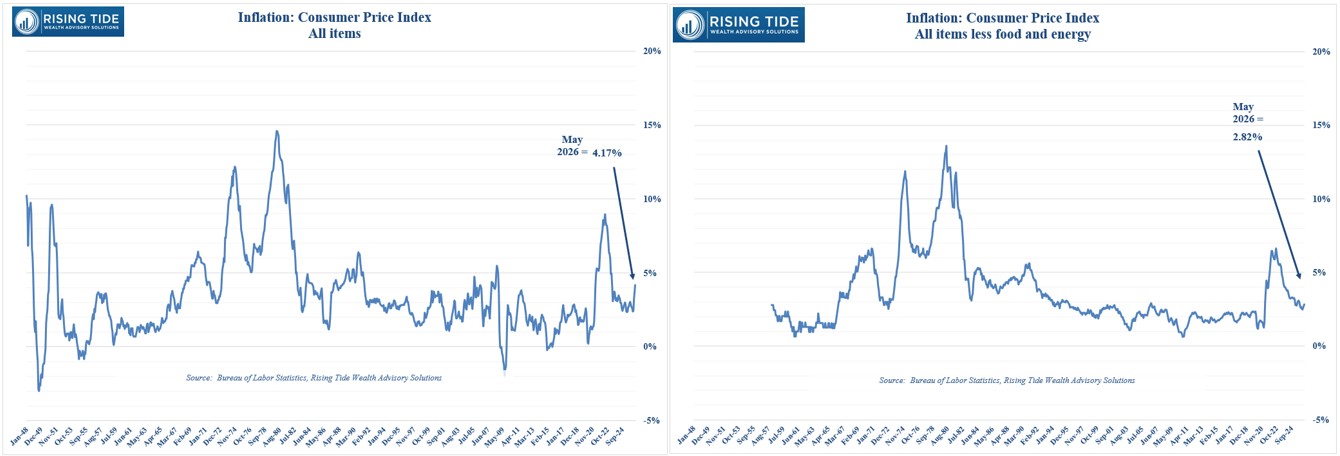

Inflation, meanwhile, moved in the opposite direction.

Headline CPI accelerated to 4.2% year over year as elevated oil prices stemming from the conflict with Iran pushed energy costs sharply higher. Energy commodities alone rose more than 40% over the past year.

Encouragingly, Core CPI (which excludes food and energy) remained much better behaved at 2.8%. While higher energy prices eventually work their way into many goods and services, underlying inflation remains considerably more stable than the headline numbers suggest.

Interest rates reflected this balancing act. The 10-year Treasury yield climbed from the beginning of the quarter until peaking near 4.67% in mid-May before retreating to roughly 4.44% by quarter end. Much of that decline reflected easing tensions surrounding the Iran conflict and falling oil prices, which have reduced concerns that higher inflation will become permanent.

Staying Focused on the Long Term

Perhaps the biggest lesson from the second quarter is that markets rarely behave the way consensus expects.

Many believed the market could not continue advancing if the Magnificent Seven stumbled. Instead, leadership broadened. Many expected geopolitical uncertainty to derail equities. Instead, the market reached new all-time highs. Many continue waiting for the "all clear" before investing. Yet history repeatedly demonstrates that markets recover long before economic headlines improve.

That does not mean risks have disappeared. Earnings expectations remain ambitious. Inflation bears watching. Geopolitical uncertainty continues.

But successful investing has never depended on accurately predicting every headline. It has depended on remaining disciplined through them. Bull markets evolve. Leadership rotates. Expectations change. Diversification remains one of the few constants.

As always, our focus remains on maintaining thoughtfully diversified portfolios designed not just for today's market leaders, but for tomorrow's as well.

Disclosures:

Unless otherwise specified, all performance references for any index or investment reflect total return, which includes price changes, interest and dividends, and are quoted in US dollar returns. Unspecified indices include: "Value stocks" = Russell 1000 Value Index; "Growth stocks" = Russell 1000 Growth Index; "Large cap stocks" = S&P 500; "Midcap stocks" = Russell Midcap Index; "Small cap stocks" = Russell 2000 Index; individual sectors = the respective sector indices within the S&P 500; "US dollar" = Federal Reserve Bank of St. Louis' Broad Trade Weighted US Dollar Index; "International Developed Market Stocks" = MSCI EAFE (Europe, Asia, Far East) Index; "International Emerging Market Stocks" = MSCI Emerging Markets Index; individual countries = the respective country indices produced by MSCI; "Short-term bonds" = Bloomberg US Govt/Credit 1-3 Yr Index; "Long-term bonds" = Bloomberg US Long Govt/Credit Float Adjusted Index; "Treasury bonds" = Bloomberg US Treasury Index; "Corporate bonds" = Bloomberg US Corporate Bond Index; "High yield bonds" = Bloomberg US Corporate High Yield Index; "Emerging market bonds" = Bloomberg EM Debt USD Aggregate Index; real estate sector indices = the respective sector indices within the FTSE NAREIT REITs Indices.

Index and investment figures quoted come from Morningstar Direct. Past performance is no indication of future results. You cannot invest directly in an index. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made will be profitable or equal the performance noted in this publication.

Rising Tide Wealth Advisory Solutions, LLC ("RTWAS") is a registered investment advisor offering advisory services in the State of Missouri and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training.

This communication is for informational purposes only and is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision. The information herein is provided "AS IS" and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Rising Tide Wealth Advisory Solutions, LLC disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.

All opinions and estimates constitute RTWAS's judgement as of the date of this communication and are subject to change without notice. RTWAS does not warrant that the information will be free from error. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall RTWAS be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the information provided herein, even if RTWAS or a RTWAS authorized representative has been advised of the possibility of such damages. Information contained herein should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.